TikTok suspended a gamification feature in the European Union following an intervention by the bloc. With attention on TikTok’s growing

LATEST NEWS

LATEST NEWS

TECHNOLOGY

TikTok pulls feature from Lite app in EU over addiction concerns

TikTok suspended a gamification feature in the European Union following an intervention by the bloc. With attention on TikTok’s growing

LG’s TV business return to profitability from Europe demand recovery, streaming

LG Electronics’ TV business has returned to profitability in the first quarter from the recovery of demand in Europe and

Mark Zuckerberg says Threads has 150 million monthly active users

Meta’s Twitter/X rival Threads is growing at a stable pace. The social network now has more than 150 million monthly

SK Hynix’s profit jump shows AI demand is going strong

SK Hynix first began supplying Nvidia with HBM chips in 2022. Image: SK Hynix South Korean memory maker SK Hynix

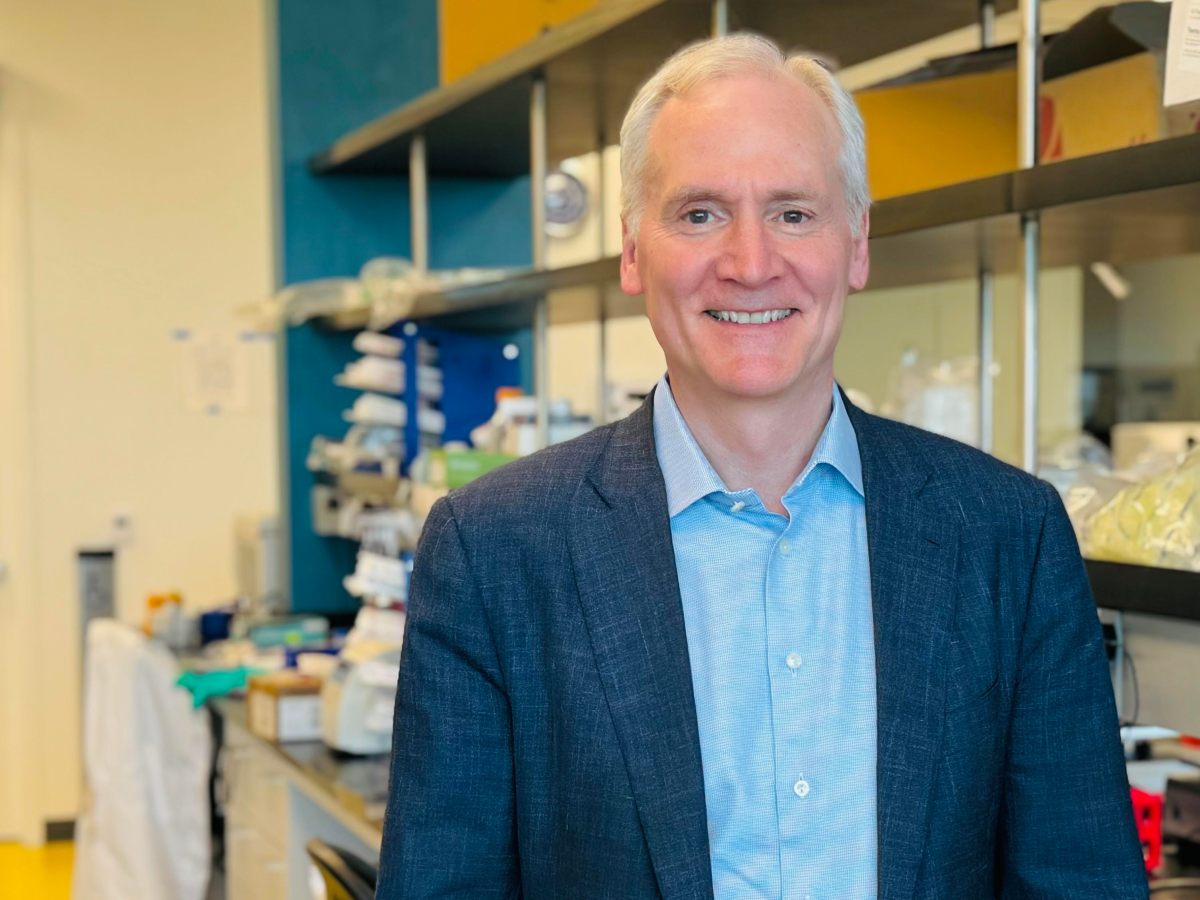

Xaira, an AI drug discovery startup, launches with a massive $1B, says it’s ‘ready’ to start developing drugs

Advances in generative AI have taken the tech world by storm. Biotech investors are making a big bet that similar

World

Klopp’s dream Liverpool sendoff spoiled by Premier League loss to Everton | Football News

Outgoing Liverpool manager apologises to fans after 0-2 loss to Everton all but dashes Premier League title hopes. Liverpool’s first