NewsFeed A new mass grave has been discovered at al-Shifa Hospital where a two-week siege by the Israeli army has

LATEST NEWS

LATEST NEWS

TECHNOLOGY

Tesla layoffs hit high performers, some departments slashed, sources say

Tesla management told employees Monday that the recent layoffs — which gutted some departments by 20% and even hit high

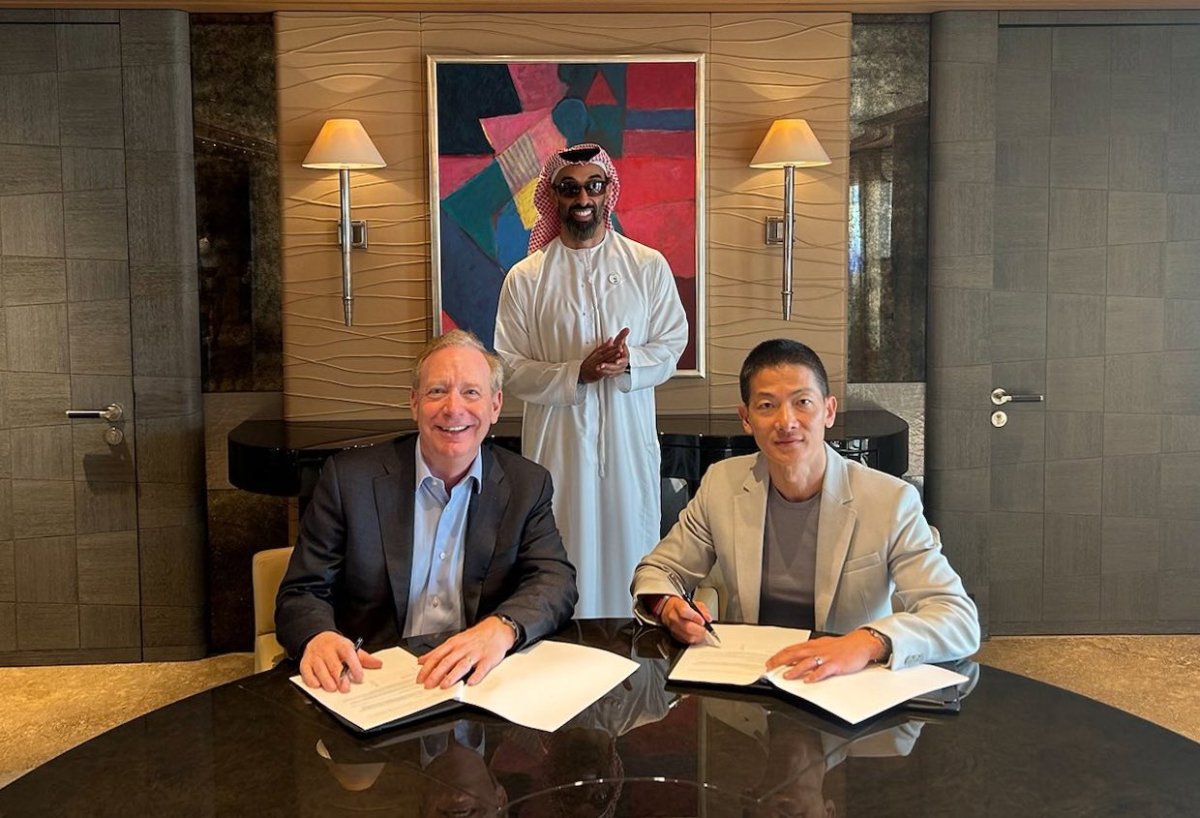

Microsoft’s $1.5B check for G42 shows growing US-China rift

As the Gulf region gains growing strategic importance for the tech war between the U.S. and China, Microsoft makes a

Big Tech’s ad transparency tools are still woeful, Mozilla research report finds

Efforts by tech giants to be more transparent about the ads they run are — at very best — still

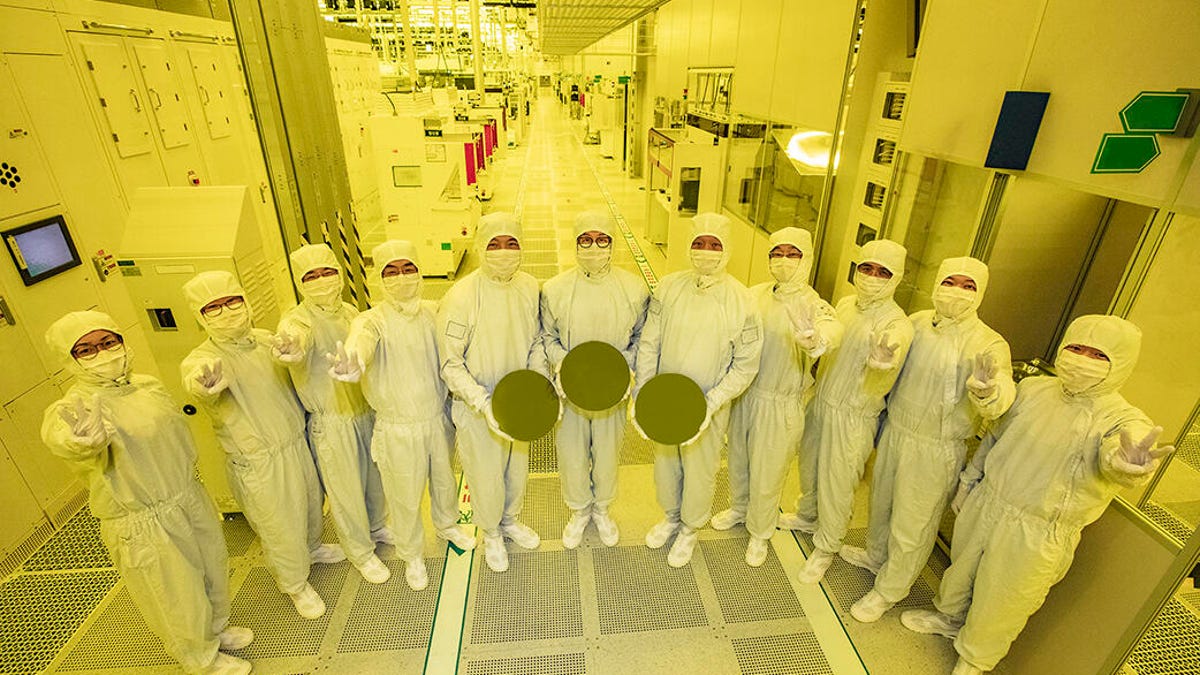

Samsung awarded $6.4 billion by U.S. under CHIPS Act to boost chip production

The U.S. government will give Samsung up to $6.4 billion in direct funding to boost its chip production in Texas,

Tesla layoffs hit high performers, some departments slashed, sources say

Tesla management told employees Monday that the recent layoffs — which gutted some departments by 20% and even hit high

World

Mass grave discovered at Gaza hospital occupied by Israeli forces | Gaza

NewsFeed A new mass grave has been discovered at al-Shifa Hospital where a two-week siege by the Israeli army has